One of our concerns throughout life is being able to maintain our lifestyle and spending power once we stop working. As time goes by, we are faced with more responsibilities and financial commitments. Mortgages, children’s education, leisure, travel and much more besides mean that, according to some studies, we spend more than 15% of our lives working.

To all this, we must add a situation in our country, in which the number of pensioners will rise considerably in the coming years, as the baby boom generation retires. According to BBVA, in September 2020 there were 1.92 persons contributing to the Social Security system for every pensioner in Spain. This ratio, known as the dependency ratio, could reach a level of 100% by the middle of the century, assuming that each person contributing to the Social Security system supports one pensioner. This shows the stress we put on our pension system, jeopardising our personal situation once we reach our expected retirement years. And what must also be added to this is a fear that is very present lately for savers: Inflation.

Average inflation in Spain over the last 30-32 years has been above 2.50%. This has meant that, had our savings been stuck in a current account rather than invested, we would have lost much of them. Specifically, in the graph below, we can see how purchasing power since the late 1980s has eroded by more than 50% due to inflation alone.

That said, and to avoid getting into these paradoxical situations where we save but lose money, it is important to consider two things. The first is that if our money is doing nothing, we will end up losing it. And the solution is its opposite: to invest. The second is to decide strategically in which assets to invest. And it is strategic because the investment we make today will provide us with a retirement in line with our expectations.

Deciding what kind of retirement we would like to have is linked to making decisions today. These decisions depend on a number of factors, which we assess below, and which help us define, in broad terms, how we should invest our savings so that they contribute, in the best possible way, to ensuring an enjoyable retirement.

Considering that risk aversion will be lower the younger we are, assuming we will have fewer financial responsibilities, it is at this time that we should invest most of our savings. We will be able to take on more volatility, we will have less need for liquidity and we should concentrate our savings efforts on acquiring positions in financial assets that can be very profitable for us. As we get older, we will generally become more cautious. We will lower our exposure in proportion to the investment, and will want to remain more liquid through larger positions in our current accounts. After retirement, we will no longer receive a large part of our income and our ability to save will also be reduced.

Another relevant decision will be the position we want to take in the capital market. We have to choose between becoming lenders, i.e. investing in monetary assets (deposits, debt, fixed income products) or being owners, which means investing in real assets, such as shares, houses, commodities or shares in a business. The difference is that while real assets imply some kind of ownership relationship and the income we get can be highly variable, monetary assets are nothing more than a promise of income payments in the future. Although they tend to be more collateralised, they are less liquid and have lower returns.

At Cobas AM, investing as asset owners seems to be more interesting to us. Historically, investment in real assets, and especially equities, has proven to be by far the best possible long-term alternative. Any other option risks incurring an opportunity cost that can be very large.

When looking for vehicles that allow us to invest in real assets, we have the option of investing in investment funds and pension plans. It is sometimes difficult to determine which product is more favourable as a future savings instrument for an investor, and we find the mixed strategy, where we have a portfolio with both options, the most interesting.

Today we are going to explore a little more in depth what pension plans are all about, so that we understand how these instruments can accompany us during our professional life in order to have the most prosperous retirement possible.

The objective of an individual pension plan is to encourage savings during our working life, benefiting from the maximum tax advantages, in order to be able to receive the accumulated capital upon retirement. This will make it possible to supplement what we receive from the state pension.

There are three main reasons why it makes sense to have a pension plan:

- The significant tax advantages they provide.

- Expectations of pension payments from the state pension.

- The long-term revaluation capacity of an accumulation pension fund.

Although the maximum amounts that can be received from the state pension today may seem sufficient, they may be much lower if one takes into account the inflation accumulated over long periods of time and the limitation that the high dependency ratio mentioned above may imply. It is therefore clear that there is a need to find ways to supplement our state pension and maintain our standard of living.

Pension plans are products designed for retirement so, as we have seen, they have tax advantages, but also certain limitations. For example, they can only begin to be redeemed 10 years after the initial contribution, unless there is a serious contingency such as disability, serious illness, long-term unemployment or death of the unitholder.

Although it is true that with the cutback in pension plans, lowering the maximum annual contribution allowed from 8,000 euros to 2,000 euros, there may be many savers who do not find it so interesting to invest in this type of financial instrument and opt for another. In my opinion, even if the ability to save through these instruments has been reduced, benefiting from the corresponding advantages, it is clear that they are still attractive because of the tax deduction. And we will have to see how employment plans will be stimulated and favoured to compensate for this drop. If we also set a routine annual contribution of 2,000 euros per year, it can end up being a very good option.

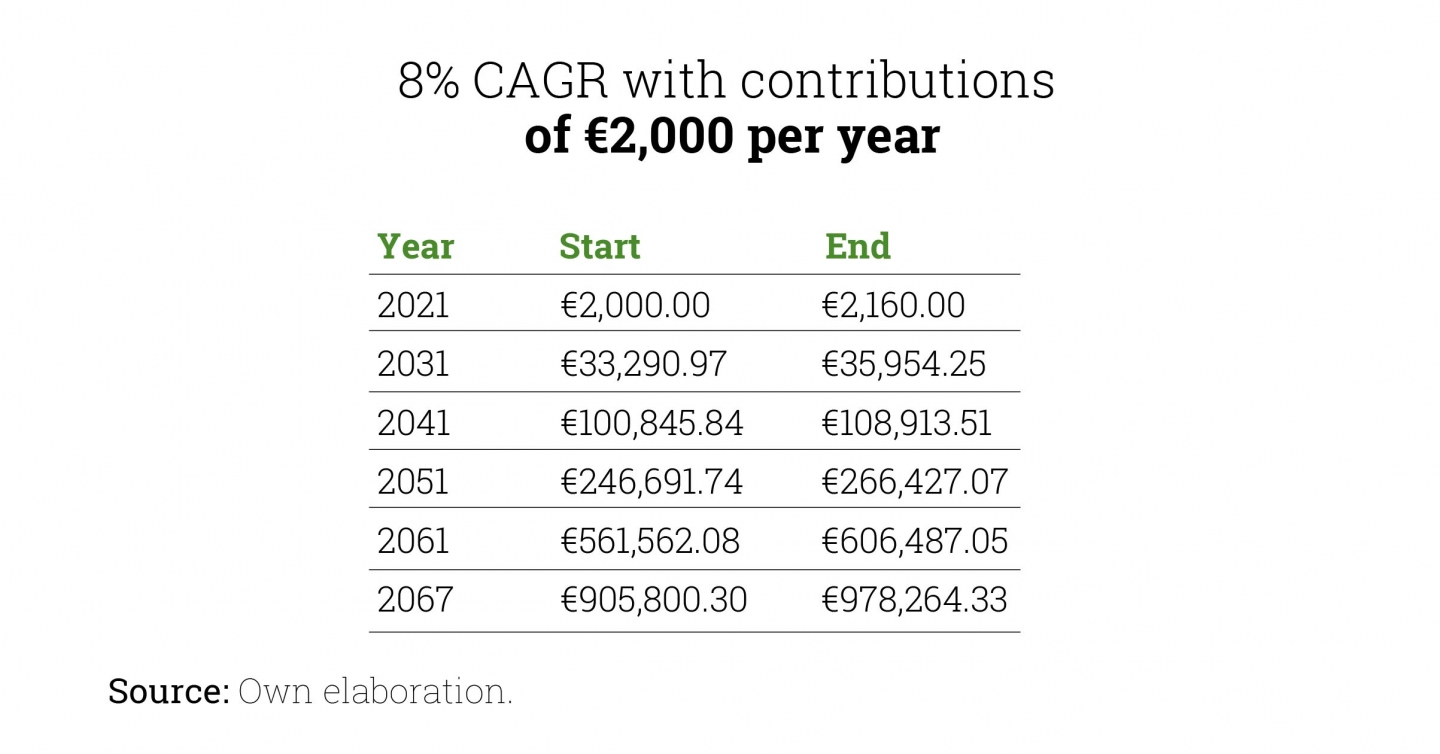

I will give you an example so that you can see how, with an annual contribution of 2,000 euros per year, it can still be interesting.

Let’s say a young saver, at the age of 18, starts making contributions to his pension plan and sets himself the objective of continuing to make these contributions, year after year, until his retirement age, obtaining an annualised return of 8%.

Contributing 2,000 euros over 47 years with an average annual return of 8%, and thanks to the exponential impact of compound interest, at retirement age, he would have an accumulated total of close to one million euros. Seen in this light, although the maximum annual contribution for pension plans has been lowered, it is still a very good option.

It is important to understand that each financial product has different characteristics – especially in terms of taxation – and it is very important, before opting for one or the other, to know in depth the implications, both in terms of contributions and redemptions, of each of them. And so, we can make the most appropriate decision depending on our personal circumstances.

At Cobas AM, we manage two pension plans. Each of them is geared to the investment time horizon that each unitholder has until the pension plan is drawn down.

– Cobas Global PP: 100% equity oriented fund. Aimed at investors with investment time horizons longer than 4-5 years.

– Cobas Mixed Global PP: More conservative. It invests between 25% and 75% of assets in equities and the remainder in fixed income assets. This plan is designed for investment horizons of at least 2, 3 or 4 years.

In short, we should think of ourselves as savers whose best interest is to make these savings profitable in order to obtain a consistent income throughout our lives. As part of this strategy, it is a prerequisite that we incorporate taxation into our investment strategy. As pension plans are a vehicle with interesting tax advantages, they should always be part of our financial planning for life.

Did you find this useful?

- |